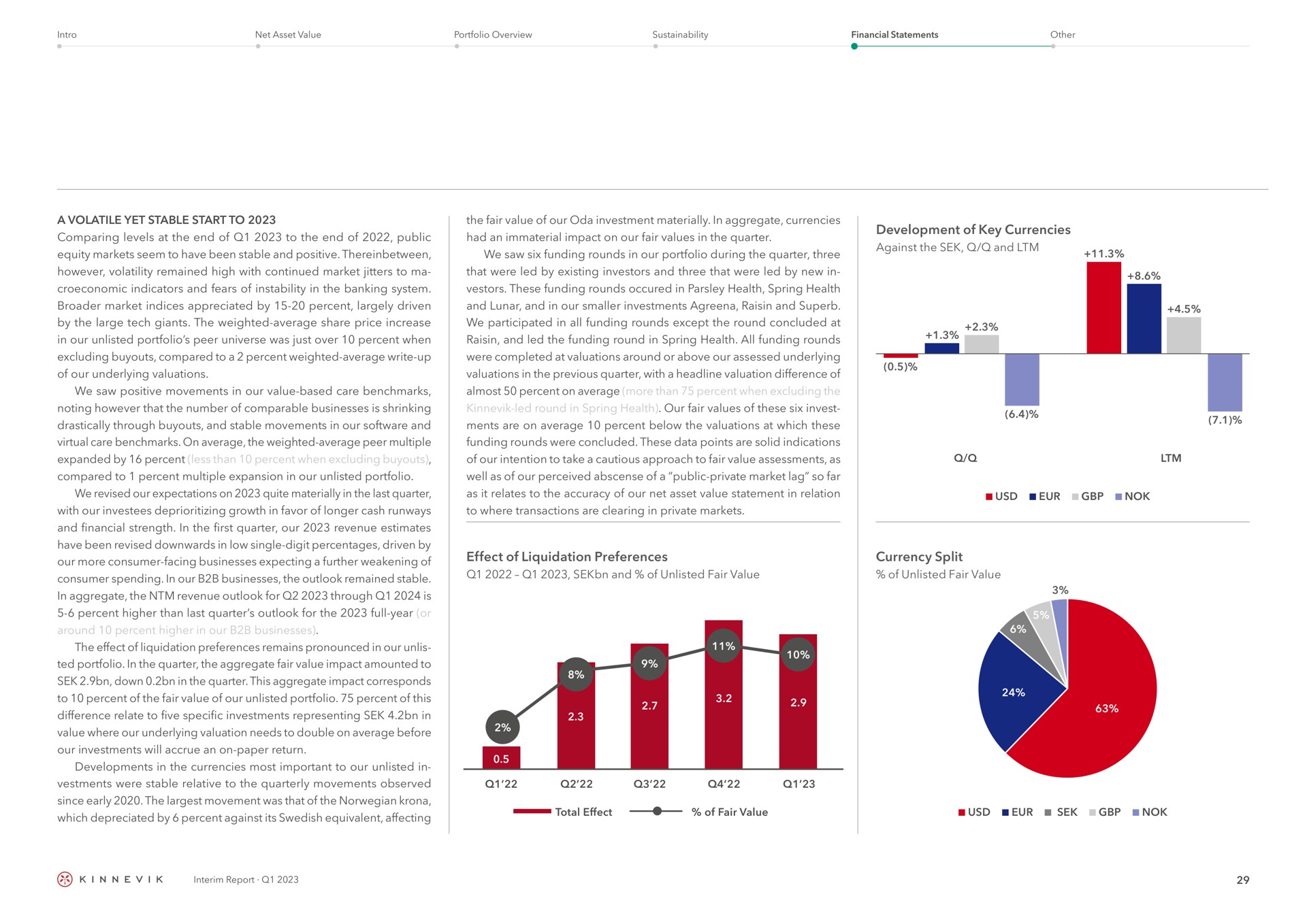

Kinnevik

Company

Deck Type

Sector

Industry

Deck date

April 2023

Slide

29 of 45

Related slides by other companies

Results

February 2024

Results

July 2023

Results

July 2021

Results

July 2023

Other recent decks by Kinnevik

Investor Day

October 2024

Results

July 2024

Results

July 2023

Results

July 2023

Search Thousands of Presentations by World Leading Companies